Investing: An Intellectual Puzzle

A guest post

Disclaimer: This is not investment advice. This article is for educational purposes only. Please consult your financial advisor and do your own due diligence before taking any decision. The writer may or may not have holdings in any companies mentioned.

Malhar is an incoming college freshman at The University of Chicago (class of 2028). He is a voracious reader and loves learning. He is deeply intellectually curious and finds investing to be a fascinating ‘intellectual puzzle’, as we will see in this post. Having begun at the age of 14, he has met several stalwarts of industry and capital markets, including Mr Rakesh Jhunjhunwala, Mr Deepak Parekh, Mr Sanjeev Bikhchandani and numerous others, and has interned with Rare Enterprises. He writes a Substack (here) about interdisciplinary mental models, where he has interviewed Ogilvy vice-chairman Mr Rory Sutherland and best-selling author Mr Jimmy Soni.

Here it goes!

Capital Cycles

I love reading on multi-disciplinary topics, but the two books that have most shaped my investment approach are Capital Returns and Zero To One. The former is about capital cycles, and the latter about (among many other things) innovative monopolies.

Zero To One raises Peter Thiel’s famous contrarian question: ‘What important truth do very few people agree with you on?’ The greatest innovations occur when one uncovers deep truths – both fundamental and emergent – that are overlooked by conventional wisdom. Thus, the contrarian question is a search for hidden secrets, and good answers to the contrarian question are the closest we can come to looking into the future.

Capital Returns, interestingly, offers an answer to the contrarian question in the context of investing, effectively saying: ‘Most investors and analysts focus on predicting demand, but the reality is that supply side analysis has greater predictive power.’ There are multiple reasons for this, including game theory, which I will not go into here.

I have had the good fortune of corresponding with Mr Neil Ostrer, co-founder of Marathon Asset Management, London, whose investment letters (officially ‘Global Investment Reviews’) have been compiled into Capital Returns. Based on my multiple readings of the book, as well as my exchange of letters with Mr Ostrer, here is my understanding of the capex to depreciation ratio.

There are two types of capex — maintenance capex (repairs and refurbishment of existing capacity) and growth capex (setting up new capacity). This has some parallels by the way: work function energy and maximum kinetic energy of electrons in the photoelectric effect; or transfer earnings and economic rent in economic wage theory.

The capital cycle approach monitors the supply side in an industry, attributing booms to shortage and busts to overinvestment. Thus, it considers growth in an industry’s capacity — through capacity addition by incumbents, fragmentation, entry of new players etc. — to be unfavourable. On the other hand, capacity leaving the industry — by consolidation, deleveraging, shutting of existing plants etc. — is favourable.

Now, it is crucial to understand that while growth capex leads to an increase in capacity, maintenance capex does not. Hence, the nature and type of capex is crucial — a high proportion of total capex going towards growth capex (at an industry level) may be a negative sign.

With depreciation serving as a proxy to maintenance capex, the capex to depreciation ratio (C/D) gauges the proportion of total capex to maintenance capex — the lower the better. If C/D is 1, for example, it suggests that all the capex undertaken pertains to maintenance capex. While there is no one-size-fits-all model, C/D of 1 or below is usually a positive sign. The way one can calculate this is,

Go to the screener page for a company —> cash flow section —> cash from investing activity —> fixed assets purchased. This will give you the capex figure.

Go to the screener page for a company —> profit & loss section —> depreciation. This will give you the depreciation figure.

Divide the first number by the second to get the C/D ratio.

Charting this ratio across time can often lead to insights on capital cycle trends.

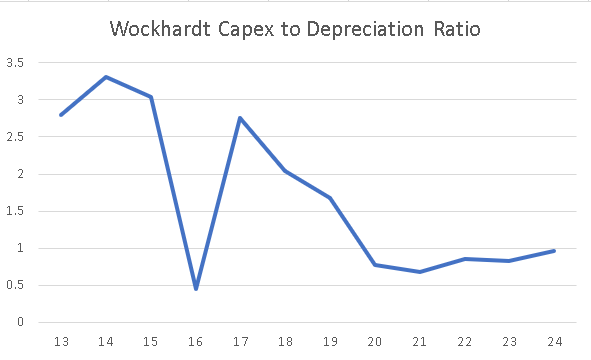

For example (please refer to the disclaimer at the start), consider how globally, large pharma companies have chronically underinvested in antibiotics R&D over the last few decades. Consequently, the global pipeline of antibiotics is narrow. At the same time, due to the ever-growing resistance mechanisms of bacteria, many of the current antibiotics are becoming less and less effective. With a favourable supply side (see this excellent report), a positive capital cycle is set to take place, in my humble opinion. In this context, consider the C/D chart for Wockhardt (below 1 in recent years).

Similarly, consider the below chart for Tilaknagar Industries.

An open question for me is, what is the equivalent of the capex to depreciation ratio in the case of banks and NBFCs? Obviously, the concepts of capex and depreciation are irrelevant in that case, and a different metric is required to gauge the supply side. My best guess would be perhaps the disbursement to provision ratio, lower the better. Thoughts on this are invited.

The key to the capital cycle approach lies in figuring out industries where this is no new supply, and ideally even a decrease in existing supply. One of the simplest ways to gauge this (apart from the quantitative ratios outlined above) is to ask, ‘what is the incentive for someone to increase supply?’ In fashionable sectors like electric vehicles, smart meters, data centers, renewable energy etc., there is all the incentive in the world for incumbents to expand and for new players to enter.

But what was the incentive in 2020-21-22 for PSU banks to grow their loan book aggressively? Absolutely none. On 9 November 2020, Tamal Bandyopadhyay published a well-written book titled Pandemonium: The Great Indian Banking Tragedy — it details the woeful stories of PSU banks, including one bank chairman suffering in jail. While most investors could see a history of bad loans, the capital cycle investor would have noticed that PSU banks have provisioned heavily. Admittedly, my analysis here is affected by hindsight bias, but this video is extremely insightful.

Similarly, this excellent video explains this point by asking,

If I’m an entrepreneur and I set up a power plant at 4 Cr per megawatt, but the market is valuing the company at 2.5 Cr per MW. As an entrepreneur, if I set up another megawatt, the market will mark it down immediately, so what is my incentive to put up a new plant?

Innovative Monopolies

Conventional economic theory says that perfect competition is the most efficient market structure: with no product differentiation or entry barriers, the threat of competition forces a company to operate efficiently. But Peter Thiel disagrees.

Thiel realises that an innovative monopolist can use its sustained profit pools (RoCE > cost of capital) to think long-term and invest in R&D and technology to strengthen entry barriers.

As an example for illustration purposes (again, please refer to the disclaimer), here is my note on Avantel.

Investing and Poker

Personally, I find these parallels between sound investing and poker styles:

Fold even slightly mediocre hands, waiting out for the hands where the odds are favourable — pass on any half-decent investment idea, betting only on the best ones.

Begin with a significant but not-too-large bet, even if you have pocket aces — allocate a moderate percentage of the portfolio to begin with.

With every revelation of cards at the table (flop, turn, river), re-assess the odds and decide bet sizing accordingly — as new information arises about a company, adjust position size dynamically (Bayesian thinking).

There are a couple of fascinating nuances to this parallel, though:

In poker, the probabilities are mechanistic/deterministic, i.e., anyone who has access to all the information as you, can construct a (hypothetical) odds table exactly equivalent to yours, since it is simply math. In investing, the interpretation of information is non-trivial; the same company disclosure or external event can be interpreted in very different ways by different people.

In poker, one cannot withdraw bets one has already made, but only choose the incremental amount to bet in every round. In investing, by selling out of a holding, one can not only refuse to invest additional capital when the odds are unfavourable, but also redeem capital already invested in a losing bet.

These two nuances make investing an even more favourable game to play than poker, in my assessment.

Calculus and Investing

Calculus is my favourite branch of mathematics — I absolutely love it. It has shaped how I think about investing — not through actual math equations, but through the underlying concepts of rate of change and area under the curve.

Stock prices are driven by delta (Δ), i.e., change and surprise. Investment decisions are in large part about the expectations embedded in the price. I would encourage you think of it in terms of reverse engineering, or ‘invert, always invert’.

At cheap valuations, prices have already anticipated and factored in most possible negatives — the question to be asked is, ‘what would be required for there to be a rise in prices?’ and likewise for a decline. When valuations are cheap, a large negative surprise would be needed for a down move, while even a small positive surprise would create an up move. The opposite is true in the case of expensive valuations.

As Mr Howard Marks writes in his 1993 memo,

At least twenty-five years ago, it was noted that stock price movements were highly correlated with changes in earnings. So people concluded that accurate forecasts of earnings were the key to making money in stocks.

It has since been realized, however, that it’s not earnings changes that cause stock price changes, but earnings changes which come as a surprise. Look in the newspaper. Some days, a company announces a doubling of earnings and its stock price jumps. Other earnings doublings don't even cause a ripple — or they prompt a decline. The key question is not “What was the change?” but rather “Was it anticipated?” Was the change accurately predicted by the consensus and thus factored into the stock price? If so, the announcement should cause little reaction. If not, the announcement should cause the stock price to rise if it is pleasant or fall if it is not.

This relates to a pet theory I have:

Probability-weighted incremental upside > Probability-weighted incremental downside,

for a sound investment

However, the reflexivity theory is worth keeping in mind. An improvement in fundamentals (say, an increase in provision coverage ratio for an NBFC) may lead to a rise in valuations (higher price to book), which in turn allows the NBFC to raise equity capital with lesser dilution — this virtuous cycle has been one of the core pieces of the Bajaj Finance story.

Anecdotally, it is evidenced that while the greatest absolute returns (multiple of initial capital) are made buying at cheap valuations, the greatest CAGR returns (absolute returns per unit time) are made in the euphoria. The difference between absolute and CAGR returns is a crucial idea to understand.

From 1993 to 1998, Infosys share price rose 100x (CAGR of ~150%), but from 1998 (when it was already ‘expensive’ by conventional measures) to 2000, it grew another 10x (CAGR of ~210%) — note how the CAGR is higher in the second case. These are staggering numbers, but most cases will show that the highest CAGR at the margin occurs during the last leg of a bull market.

Terminal Value

When Peter Thiel ran some projections in 2001, he realised that 75% of PayPal’s value would come from cash flows generated after 2011. Terminal value drives the majority of net present value for any growing cash flow stream — and, after all, the value of any company is the NPV of all future cash flows, appropriately discounted.

Similarly, when Elon Musk says that he expects Optimus to drive the majority of Tesla’s long term value, it is terminal value to which he is referring.

Terminal value is driven by growth and durability — the compounding formula is driven by rate of return (growth) and longevity of time period (durability).

Quality of growth is paramount. Growth contributes positively towards terminal value only when return on capital employed exceeds cost of capital. Thus, RoCE and growth, together with durability of this combination, are ideal ingredients for value creation.

While most analysts focus on short-term growth, the more important question to ask is, ‘will this firm be around 10 years from now?’ The best answers to this question arise not by crunching numbers but through an understanding of intangibles — especially enduring intangibles like people and culture.

One way to gain an appreciation for such intangibles is by reading historical annual reports of wealth creators (and destroyers). Again, hindsight bias is likely to creep in, but it is a valuable exercise to read, say, the annual reports of Titan from 2003 onwards, or the reports for Page Industries from 2010 onwards — as you do so, try to place yourself in the shoes of someone evaluating the company at that time, and make note of your observations. I have done so extensively, and attached my learnings below.

I could go on and on, but I will stop for now. I would greatly appreciate your feedback, either in comments or over email (malhar.manek@gmail.com) — you might also enjoy reading posts on my blog!